UK Chancellor's Tax Dilemma: Balancing Pragmatism and Policy

Chancellor Rachel Reeves faces tough decisions on tax policy, limited by pre-election pledges. Historical examples show the potential for unintended consequences in tax reforms, highlighting the need for careful consideration.

Chancellor Rachel Reeves finds herself in a challenging position as she prepares for the upcoming Budget on October 30, 2024. The task of reforming the UK's intricate tax system while adhering to pre-election commitments has created a significant dilemma.

The complexity of the UK's tax structure, considered one of the most intricate globally, demands comprehensive reforms. However, Reeves' pledge to avoid increases in income tax, National Insurance, and VAT has severely restricted her options. These taxes, introduced in the UK at various points since 1799, 1911, and 1973 respectively, represent the largest sources of government revenue.

This limitation forces the Chancellor to focus on smaller, potentially less efficient taxes, which may result in more public discontent and unintended consequences. Historical examples illustrate the risks associated with hasty or poorly considered tax decisions:

- In March 1988, Chancellor Nigel Lawson's pre-announced ending of multiple mortgage tax relief led to a property boom and subsequent crash.

- Gordon Brown's 1997 abolition of the dividend tax credit for pension funds, introduced in 1973, resulted in significant long-term losses for pensioners and reduced institutional investment in UK companies.

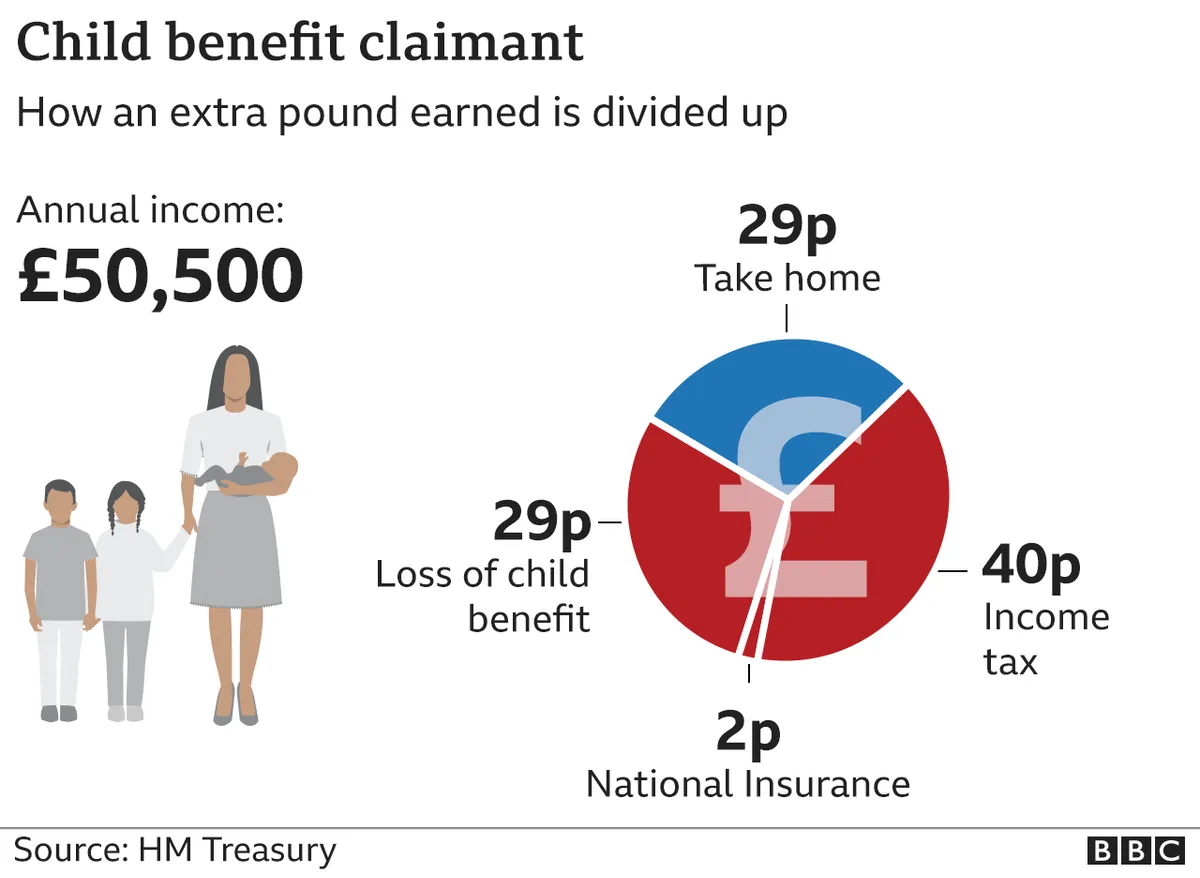

- Alistair Darling's 2009 decision to reduce the personal income tax allowance for high earners created an effective 60% tax band, causing generational unfairness.

"The art of taxation consists in so plucking the goose as to obtain the largest possible amount of feathers with the smallest possible amount of hissing."

The introduction of VAT on private school fees, set to take effect in January 2025, exemplifies the potential for unintended consequences. In Surrey, one of England's most affluent counties, this could lead to a significant influx of students into already strained state schools.

Speculation about potential changes to Capital Gains Tax (CGT), introduced in 1965, raises concerns about the impact on the buy-to-let market and housing availability. Similarly, alterations to pension tax treatment could discourage prudent retirement planning, potentially increasing reliance on state support in later years.

As George Bernard Shaw, co-founder of the London School of Economics, astutely observed, "A government which robs Peter to pay Paul can always count on Paul's support." However, the challenge for Reeves lies in crafting policies that are not only politically expedient but also economically sound and fair across generations.

The upcoming Budget presents an opportunity for the Chancellor to prioritize prudent policy over short-term pragmatism, ensuring that any tax reforms consider both immediate impacts and long-term consequences for the UK's economic landscape.