UK Chancellor Faces Pressure to Slash Tax-Free Pension Withdrawals

Proposals to cap tax-free pension withdrawals at £100,000 could raise £2bn but face implementation challenges. The move aims to address wealth inequality in the current system.

Rachel Reeves, the UK Chancellor, is facing mounting pressure to implement significant changes to the pension system. The Institute for Fiscal Studies (IFS) has proposed capping tax-free pension withdrawals at £100,000, a move that could potentially generate £2 billion in revenue.

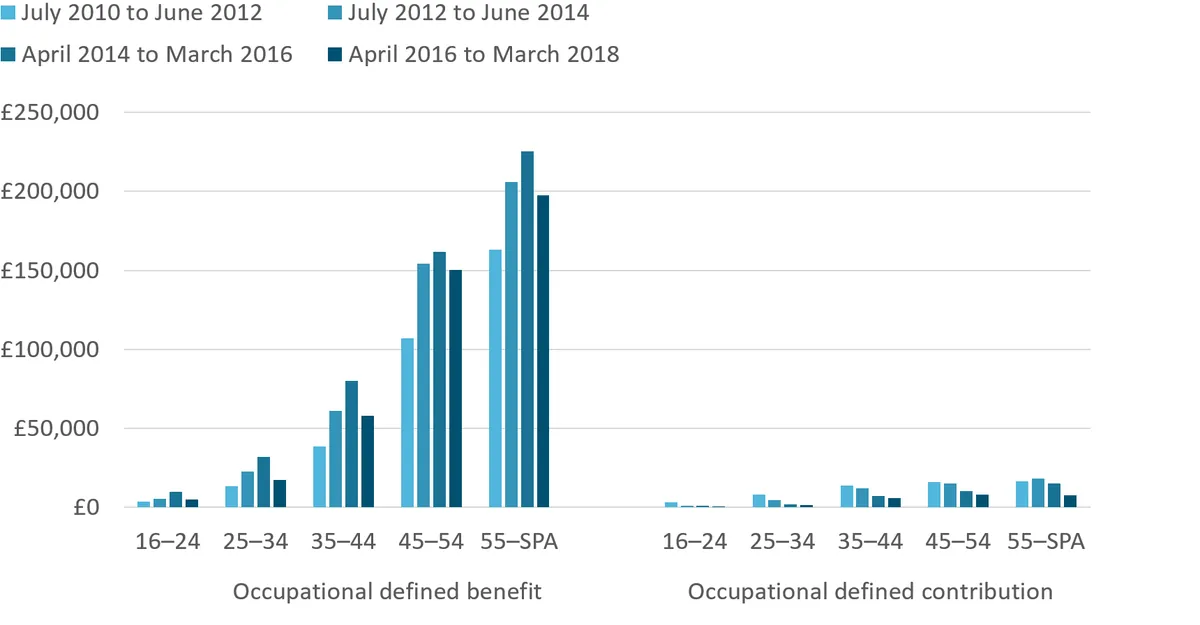

Currently, individuals can withdraw up to 25% of their pension pot tax-free upon reaching the age of 55, with a maximum limit of £286,275. This system, introduced in 2006 by then-Chancellor Gordon Brown, has been criticized for disproportionately benefiting high earners.

The UK pension system, which dates back to 1908, has undergone numerous changes over the years. Despite ranking 9th globally in the Mercer CFA Institute Global Pension Index, the UK state pension remains one of the lowest among developed countries. Only 27% of UK adults feel confident about their retirement savings, highlighting the need for reform.

The proposed changes would affect approximately one in five retirees, primarily those with pension pots worth around £1 million. The IFS argues that the current system's support for this group is "hard to justify" and suggests redirecting some of the revenue to boost the pensions of low-income individuals.

Implementing such changes, however, presents significant challenges. Sir Steve Webb, a former pensions minister, emphasized the need for transitional arrangements:

"Implementing a much lower cap would be far from straightforward. Those who had already built up rights to a substantial lump sum might feel very aggrieved if the rules were changed at the last minute."

The proposal also faces potential criticism regarding its impact on long-term savers and the risk of generating limited short-term revenue after accounting for transitional measures.

As the UK grapples with an aging population and a projected 40% increase in people aged 65 and over in the next five decades, pension reform remains a critical issue. The government currently spends about 5.5% of GDP on pensions, and any changes to the system must balance fiscal responsibility with the needs of retirees.

The debate surrounding tax-free pension withdrawals highlights broader issues in the UK pension landscape, including the gender pension gap of around 40% and the success of auto-enrollment, which has brought over 10 million people into workplace pension schemes since its introduction in 2012.

As discussions continue, the Chancellor must weigh the potential benefits of increased revenue and reduced wealth inequality against the challenges of implementation and the risk of alienating long-term savers.