UK Treasury Faces Mounting Debt as Budget Looms

As Rachel Reeves prepares her first Budget, the UK Treasury is set to borrow heavily. Public debt nears economy's size, with borrowing overshooting targets amid increased spending and weaker tax receipts.

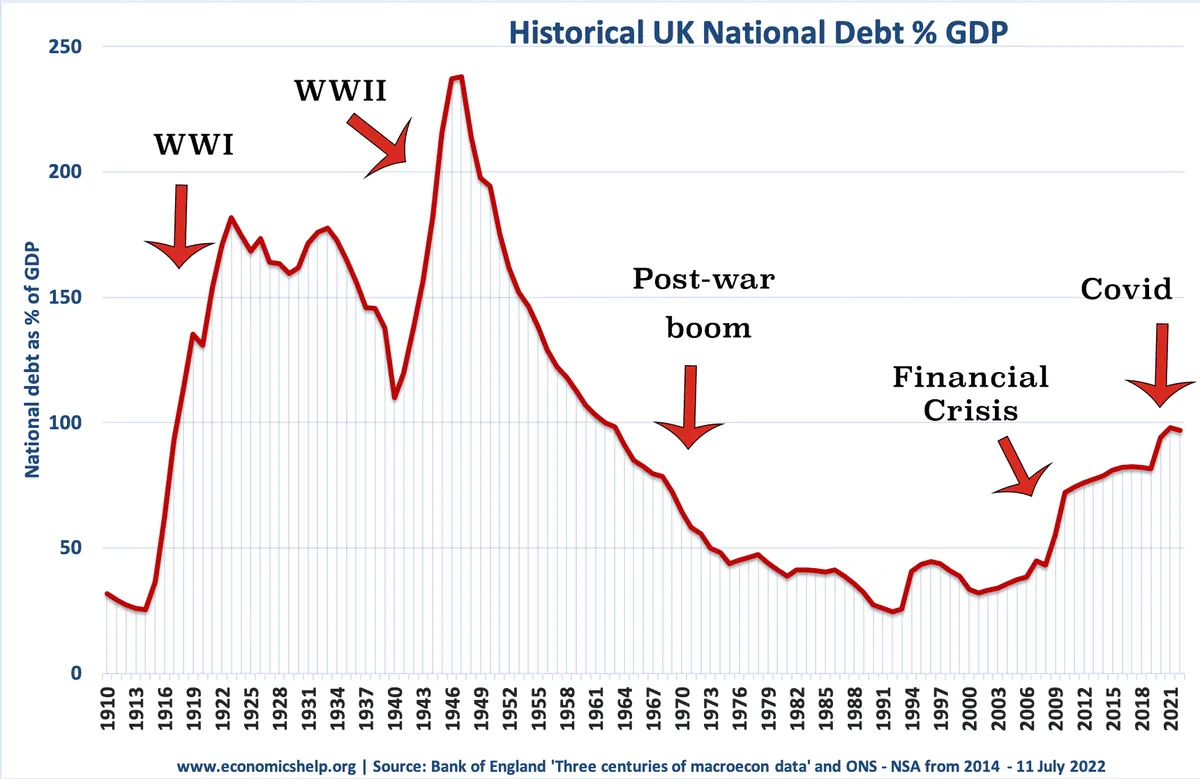

As Rachel Reeves prepares to deliver her inaugural Budget, the UK Treasury finds itself on a trajectory to borrow substantial sums over the coming five-year period. The current fiscal year alone is projected to exceed the borrowing target established merely six months prior, primarily due to increased public expenditure. The nation's total debt has now reached parity with its economic output.

Recent public borrowing data revealed that the Treasury has borrowed £6.2 billion more than the Office for Budget Responsibility (OBR) had anticipated for this financial year. The OBR, an independent fiscal watchdog established in 2010, plays a crucial role in monitoring government finances. When considering the cash requirement metric, which the Treasury uses to determine gilt issuance, the overshoot is even more significant at £16.7 billion.

The issuance of gilts, a practice dating back to the late 17th century, has seen a marked increase since the pandemic. This trend is likely to continue as the Chancellor addresses what she terms a £22 billion deficit inherited from the previous administration. While Reeves has indicated that difficult decisions lie ahead in her upcoming Budget, any changes will come too late to prevent the need for additional borrowing in the current fiscal year.

The Debt Management Office (DMO), established in 1998 to manage government debt, may need to access financial markets for hundreds of billions of pounds this year alone. This includes rolling over existing debt and issuing new bonds. Economists project that gilt issuance could exceed £300 billion for the fiscal year, surpassing previous estimates.

Several factors are contributing to the increased borrowing and debt. These include inflation-exceeding public sector pay agreements, diminished tax receipts, and compensation costs related to the infected blood inquiry initiated in 2017 and the Post Office scandal involving wrongful convictions of subpostmasters. Additionally, the government's ambition to attract more savings through National Savings and Investments (NS&I), a state-owned savings bank founded in 1861, has fallen short of expectations.

Despite the high levels of borrowing, demand for UK debt remains robust. The average number of bids for each bond offered by the DMO increased to 2.78 last year, up from 2.39 the previous year. This strong appetite is partly attributed to higher yields making gilts more attractive and a perception of relative political stability in the UK compared to some other nations.

"I believe [strong demand] will continue as long as you have what is perceived to be a plan and a competent Chancellor, especially when you compare us to other countries."

However, the rising debt levels present challenges. The UK's debt-to-GDP ratio, which exceeded 100% for the first time since 1961 in 2020, could climb further if public spending continues to increase. The Lords' Economic Affairs Committee, established in 2001, has warned that the Chancellor must either raise taxes or reduce public services to mitigate the risk of a potential debt crisis.

As speculation mounts about potential tax changes, experts suggest that Capital Gains Tax (CGT) and Inheritance Tax (IHT) could be targets for increases, given Reeves' commitment to avoid raising income tax, VAT, National Insurance contributions, and corporation tax. Any alterations to the tax treatment of gilts could impact investor appetite, potentially affecting the government's ability to borrow.

The upcoming Budget will be closely watched for signals of fiscal discipline and any changes to debt rules. As the debt continues to rise, the Chancellor faces the challenge of balancing economic growth with sustainable public finances in an environment of higher borrowing costs and global economic uncertainties.